This paper explores three plausible future scenarios for scaling Carbon Dioxide Removal (CDR). Drawing on current trends, emerging weak signals (early, often subtle or fragmented indicators of emerging change that may later develop into significant trends or issues), signposts (observable events or indicators that show how trends or scenarios are developing over time), and social, technological and policy drivers, the scenarios examine how governance pathways could evolve across international institutions, national governments, subnational authorities and private-sector actors. Rather than predicting specific outcomes, the analysis offers foresight into potential trajectories of global CDR governance and highlights risks and opportunities that could shape more equitable and effective carbon removal strategies, recognizing differences in capacity, historical responsibility and development priorities between the Global North and Global South.

Introduction

Carbon dioxide removal (CDR) is an increasingly important part of global climate mitigation strategies. Even under ambitious decarbonization pathways, some emissions from hard-to-abate sectors such as cement, aviation and heavy industry are expected to persist.1 Limiting warming to 1.5°C or well below 2°C generally requires CDR to offset these residual emissions, with many mitigation pathways assuming net-negative emissions later in the century.2

Historically, carbon removal has been dominated by land-based approaches such as afforestation, reforestation and soil carbon sequestration. Today, roughly two gigatonnes of CO₂ are removed annually, almost entirely through land-based practices, which are constrained by land competition, ecological limits and concerns about permanence, as stored carbon can be reversed through disturbances such as wildfire or land-use change. Novel methods such as direct air carbon capture and storage (DACCS), bioenergy with carbon capture and storage (BECCS) and enhanced weathering depend on engineered systems to remove and store carbon in geological or mineral forms, offering greater durability but with limited infrastructure and at a higher cost.3 These methods currently contribute about 1.3 megatonnes of carbon removals, less than 0.1 percent of total removals. Achieving Paris-aligned targets of seven to nine gigatonnes per year by 2050 will therefore require rapid technological scaling, alongside supportive governance frameworks.4

The gap between current removal capacity and climate targets reflects what has been described as a “gray rhino,” a highly probable, high-impact and visible threat that gives clear warning signs, yet remains insufficiently addressed due to political and institutional inertia until it escalates into a crisis.5 Warning signs, including low technology deployment, insufficient policy frameworks and persistent residual emissions, have been evident for years, yet meaningful action to close the gap remains limited.

Over the past two decades, CDR has moved from a largely theoretical component of climate models to a growing area of technological innovation and policy experimentation. Early models highlighted options such as BECCS, while more recent advances and private investment have accelerated interest in direct air capture (DAC).6 However, first-generation DACs remain costly — between $600 and $1,000 per tonne, far more than the less than $200 per tonne assumed in many net-zero pathways.7 These challenges highlight the importance of sustained policy support and coordinated governance.

Policy development for CDR is uneven and shaped by broader energy politics. The United States reflects both expansion and political volatility in this regard. The Bipartisan Infrastructure Law and the Inflation Reduction Act strengthened the Section 45Q tax credit for regional DAC hubs to scale CO₂ capture, transport and storage infrastructure.8 Yet recent legislation has also expanded fossil fuel subsidies by an estimated $3.5 billion annually, in addition to the roughly $31 billion already provided, highlighting persistent policy contradictions.9 Moreover, political volatility, including the temporary US withdrawal from the Paris Agreement under President Donald Trump, further demonstrates how domestic political shifts can weaken multilateral climate commitments and create uncertainty for long-term decarbonization strategies.10

Other jurisdictions are beginning to develop more structured approaches. In 2026, the European Union launched the Carbon Removal Certification Framework, establishing standards for permanent carbon removals and MRV (measurement, reporting and verification).11 The United Kingdom also plans to integrate BECCS and DACCS into its Emissions Trading Scheme, although current deployment remains below the planned target.12 Globally, most governments continue to address CDR within existing climate and energy policies rather than through dedicated governance frameworks, resulting in fragmented regulations and limited coordination.13 At the same time, advocacy networks and industry coalitions are increasingly active in shaping policy debates. Organizations such as the Carbon Removal Alliance and Carbon Removal Canada are working to bridge the gap between technological innovation and commercial deployment.14 Public awareness of carbon removal remains limited but is growing. A 2025 Abacus Data survey found that 64 percent of respondents support carbon removal technologies, although support depends on transparency, local consultation and the principle that removals should complement, not replace, emissions reductions.15

Addressing this governance gap requires a shift from reactive policy to strategic foresight. Foresight is critical in policymaking because it allows decision makers to anticipate emerging risks and opportunities, explore alternative futures, and design strategies that remain robust under uncertainty.16 By monitoring weak signals, identifying key drivers, and tracking signposts, policymakers can better prepare for complex transitions.17

This paper explores three plausible future scenarios for scaling CDR. Drawing on current trends, emerging weak signals (early, often subtle or fragmented indicators of emerging change that may later develop into significant trends or issues),18 signposts (observable events or indicators that show how trends or scenarios are developing over time),19 and social, technological and policy drivers, the scenarios examine how governance pathways could evolve across international institutions, national governments, subnational authorities and private-sector actors. Rather than predicting specific outcomes, the analysis offers foresight into potential trajectories of global CDR governance and highlights risks and opportunities that could shape more equitable and effective carbon removal strategies, recognizing differences in capacity, historical responsibility and development priorities between the Global North and Global South.

Three Plausible Scenarios

This section explores three plausible futures for CDR governance to 2050: centralized governance and coordinated global action; fragmented innovation and regional hubs; and a market-driven, technology-led race. These scenarios offer frameworks to assess how governance, stakeholder alignment and market dynamics may influence the scale, equity and integrity of global CDR deployment.

SCENARIO 1

Centralized Governance and Coordinated Global Action for Carbon Removal

This scenario envisions a transition from fragmented efforts to centralized oversight through a new multilateral framework, to be known as the Global Carbon Removal Accord, emerging by the late 2030s. As carbon removal scales, the need for common MRV standards and rules to prevent double counting (claiming the same carbon removal by multiple parties) may push actors toward alignment to maintain credibility and environmental integrity. Growing reliance on CDR in net-zero strategies, expanding voluntary and compliance carbon markets, and increasing private and regional initiatives may further incentivize governance coordination.

While not guaranteed in today’s fragmented geopolitical context, these structural pressures could still encourage coordination by suggesting international cooperation, policy alignment and institutional innovation that make large-scale CDR feasible, accountable and just. The timeline below traces this scenario from early signs of fragmentation in 2025, through key risks and outcomes, to a turning point in 2038 with the adoption of the global accord, culminating in a coordinated and unified framework by 2050

2025–2030: Early Fragmentation

Governance remains fragmented. China’s top-down system enables policy alignment but struggles with landholder engagement; the United States relies on market-driven incentives, producing uneven and inconsistent standards; and the European Union’s Land Use, Land-Use Change and Forestry Regulation establishes national targets for net carbon removals, harmonized monitoring and reporting requirements, and compliance mechanisms20 and carbon-farming schemes without fully coordinated national strategies.21

Weak signals include uneven voluntary markets, corporate concentration (the United States represents roughly 80 percent of purchased volume, and other buyers and suppliers are located across Europe, South America and Asia22) and diverse certification standards. For instance, the model of the European Commission’s Carbon Removal Certification Framework hints toward a need for centralized governance on CDR.23

Technological progress continues, yet the absence of unified standards and equitable governance deepens fragmentation. Policy and technological leadership remain concentrated in Europe, the United States and Japan, while Global South participation remains limited.24 Persistent gaps, in particular the absence of a universal MRV system, undermine the environmental integrity and trustworthiness of removal claims, increasing risks of double counting or overestimation of removals.25 The competing regional regimes, including the EU’s Carbon Removal Certification Framework and the US Department of Energy protocols, along with divergent certification requirements, further weaken market confidence26 and complicate coordination.

Together, these institutional and governance gaps interact with emerging social tensions to reinforce fragmentation across political, market and societal dimensions. Land-intensive CDR, such as BECCS and large-scale afforestation, face growing resistance from Indigenous communities and Global South actors concerned about land rights, sovereignty and the reproduction of colonial dynamics in “green” initiatives. These tensions are reflected in controversies over carbon offset and land-based carbon projects in countries such as Kenya and Liberia, as well as the large-scale conversion of community lands for carbon plantations across multiple regions.27

These concerns are further amplified by opaque technology transfer, restrictive IP regimes (that can limit access to climate technologies through patent and licensing barriers, particularly in developing countries) and conditional finance.28 These dynamics highlight the risks of fragmented governance and underscore the need for more coordinated and equitable global approaches to ensure credible, socially just and scalable deployment of CDR.

2031–2035: Fragmentation Risks

By 2031–2035, the global CDR system could reach a critical juncture as pressures for coordination begin to emerge. Advances in MRV technologies (including platforms such as Sylvera and FLINTpro) support standardized data collection, outcome tracking and independent verification, thereby strengthening measurement and reporting systems. Large-scale financing initiatives, harmonized data standards and emerging coordination platforms, such as Switzerland’s Carbon Removal Platform and the Coalition to Grow Carbon Markets, seek to reduce transaction costs and enhance transparency, accountability and credibility across global voluntary carbon market projects. These developments also support developing-country participation through capacity building and technology transfer, while improved monitoring increasingly aims to safeguard Indigenous rights and land use governance.29

In response to growing legitimacy concerns, informal coordination efforts begin to emerge, including Free, Prior and Informed Consent (FPIC), which requires states to consult Indigenous peoples and obtain their consent before adopting measures or approving projects affecting their lands and resources,30 alongside more equitable benefit-sharing mechanisms. These efforts represent early attempts to rebuild trust and strengthen governance of CDR initiatives.31 In this sense, the accumulation of governance gaps, social tensions and market credibility concerns may begin to transform fragmentation itself into a driver of coordination.

2036–2040: A Turning Point — Global Accord for Carbon Removal

By 2038, a breakthrough may occur with the negotiation of a Global Accord for Carbon Removal under the United Nations Framework Convention on Climate Change (UNFCCC). Modelled on the Paris Agreement, but with stronger institutional authority, the accord establishes binding national CDR targets, harmonized certification rules and a centralized Global CDR Authority for large-scale carbon removal. The authority operates with a governing council of member states, a scientific advisory panel and an independent MRV registry overseeing global removal credits. Compliance provisions restrict market participation for double counting or non-compliance, while incentives such as concessional finance, technology transfer and access to international carbon markets support participation by developing countries. In this framework, CDR is explicitly framed as complementary to emissions reductions. The regime embeds safeguards including FPIC, land-tenure protections, biodiversity safeguards and equity, while standardized certification and monitoring systems help reduce transaction costs and strengthen the credibility of global carbon removal markets.

Positive signposts may include growing efforts to align carbon pricing and reduce trade disputes. Rising fragmentation pressures from more than 70 divergent carbon pricing systems prompt institutions such as the World Trade Organization (WTO), the World Bank, the Organisation for Economic Co-operation and Development (OECD) and the International Monetary Fund to coordinate markets and support developing economies.32 Innovation may also accelerate in emerging CDR approaches supported by public research and EU frameworks such as MARVIC for ocean-based MRV.33 At the same time, strengthening Article 6.4 mechanisms under the Paris Agreement, which support international carbon market cooperation through standardized accounting, verification and trading rules, alongside EU certification systems, may strengthen transparency and reinforce the credibility of global carbon markets.34

2041–2050: Institutionalization and Equitable Scaling

The 2040s see the Global CDR Authority evolve into a full governance body, analogous to the WTO, with enforceable compliance, independent verification and structured dispute resolution. MRV systems advance through satellite monitoring, AI modelling and blockchain verification, reducing uncertainty and operational costs, and strengthening market integrity.35 These provide the backbone for large-scale, high-integrity markets.

Equity remains central: a Global CDR Access Fund channels finance, technology and institutional support to low-income and climate-vulnerable states, while FPIC-compliant frameworks elevate Indigenous leadership and safeguard land rights. Small Island Developing States and Least Developed Countries co-develop DAC hubs with high-income partners, linking climate justice with green industrialization pathways.36 Global cooperation, policy learning and technology transfer become essential to ensuring that scaling does not exacerbate historical asymmetries. By 2050, more than 75 countries will integrate CDR into long-term mitigation strategies, achieving average annual removals of approximately nine gigatonnes. Convergence of voluntary and compliance markets enables standardized, cross-border credits, embedding carbon removal as a routine mitigation tool.

The push for a Global Accord for Carbon Removal by 2038 reflects both climate urgency and the need to stabilize a fragmented global system. In a geopolitical environment marked by energy weaponization, cyber tensions and intensifying great-power competition, evident during periods such as the second Trump administration in the United States, the establishment of a centralized CDR authority may appear unlikely. Yet this scenario shows that scaling carbon removal depends as much on governance as on technology. By mid-century, a Global CDR Authority serves as a guarantor of quality and accountability, preventing market failure through double counting or social resistance. The core lesson is clear: the most critical breakthrough in scaling carbon removal is not technological, but institutional.

SCENARIO 2

Fragmented Innovation and Regional Hubs — Disparate Pathways

This scenario envisions CDR developing through decentralized and regionally differentiated strategies rather than a unified global framework. Early governance gaps, as well as differences in national capacities, technological strengths, policy priorities and financial resources, create incentives for countries and regional blocs to pursue strategies tailored to their own circumstances. Without strong global coordination or binding international mandates, these differences reinforce fragmented pathways: some regions focus on land-based solutions, others on technology-intensive approaches, while financing, regulatory oversight and monitoring standards diverge.

Over time, this fragmentation may persist or produce limited convergence as blocs experiment with interoperable systems, but the overall trajectory emphasizes bottom-up innovation and regionally specific governance, highlighting both the opportunities and risks of a world shaped by uneven carbon removal deployment. The timeline traces this pathway from early divergence in the 2020s to entrenched regional approaches and either persistent fragmentation or selective convergence by 2050.

2021–2023: Early Signals and Foundational Divergence

Between 2021 and 2023, the global CDR landscape began to fragment (drivers). The Paris Agreement set broad mitigation goals but lacked binding commitments for carbon removal, leaving countries to pursue national priorities, often favouring land-based approaches such as afforestation and soil carbon enhancement due to their relative maturity, lower cost, ease of monitoring, integration within existing land-use and carbon accounting systems, and fewer technological and governance uncertainties compared to emerging ocean-based methods.37 This divergence underscores the absence of a unified governance framework and the widening gap in national CDR ambitions.

By 2025, the third round of the UNFCCC’s nationally determined contributions (NDCs) (that is, national climate action plans submitted under Article 4 of the Paris Agreement and updated every five years to reflect progressively stronger ambition38), fewer than 20 countries included explicit CDR commitments.39 Trust in institutions also fell sharply, with OECD surveys reporting only 39 percent confidence in governments, alongside declining UN favourability and broader evidence of weakening trust in multilateral cooperation, amid rising anti-global narratives in Europe and the United States.40

At the same time, signposts include debates that intensified over the legitimacy, ethics and monitoring of CDR, including concerns about moral hazard (a trade-off between future CDR and present initiatives to reduce emissions), verification uncertainty and legal ambiguities (no clear international standard for CDR) in integrating removal into NDCs. These tensions are further shaped by developing countries’ resistance to equal CDR obligations under the Common but Differentiated Responsibility (CBDR) principle, alongside contestation by more than 100 organizations challenging the UN climate panel’s guidance on carbon removal credits.41

These signals indicate that early governance gaps and declining trust in multilateral institutions may steer CDR development toward decentralized regional pathways rather than globally coordinated deployment.

2024–2030: Policy Divergence and Regional Blocs

Trust between the Global North and South eroded as countries pursued divergent CDR strategies aligned with domestic economic strengths, industrial capacities and political priorities, creating a fragmented international landscape. Sweden and Denmark reinforced BECCS through their robust forestry and bioeconomy frameworks. At the same time, the United States expanded DACCS, leveraging geological storage potential, industrial capacity and federal incentives of the Inflation Reduction Act’s $180 per tonne tax credits, preserved under the 2025 One Big Beautiful Bill Act and available to projects commencing construction before 2033, with a 12-year credit duration. The United Kingdom adopted a blended DAC-BECCS approach, and Japan advanced experimental DACCS projects, emphasizing storage infrastructure, innovation and international technical collaboration.42

Early governance divergence emerged across international negotiations, civil society and corporate markets. In 2024, COP29 of the UNFCCC revealed fractured financial commitments, as developing countries criticized delayed climate finance and questioned the credibility of new pledges amid the legacy of unmet US$100 billion commitments.43 At the same time, Indigenous and civil society movements opposed land-intensive CDR removals, emphasizing FPIC, rights-based stewardship and local governance.44 Concerns over rising land prices, declining smallholder access, pressure on local food systems and water resources, and instances of “green grabbing” linked to afforestation and offset schemes further amplified equity concerns and strengthened calls for decentralized, community-led approaches.45

By the late 2020s, regional CDR blocs emerged: Nordic countries and the United States aligned MRV and storage; Japan and South Korea strengthened innovation partnerships; Brazil and South Africa pursued ecosystem-based removals, despite funding and verification gaps. Fragmented policies intensified geopolitical tensions and distributional inequities, as technologically and financially advantaged states increasingly shaped emerging standards while many lower-income countries primarily served as implementation sites without equitable benefits. Divergent regional approaches also created isolated technological pathways, hindered knowledge transfer, and prevented the realization of global economies of scale, significantly increasing double-counting risks and transaction costs.

In this context, climate diplomacy could shift from universal rulemaking toward transactional, bloc-aligned negotiations centred on bilateral or regional CDR arrangements rather than comprehensive global agreements.

2031–2040: Entrenched Fragmentation and Governance Asymmetries

During the 2030s, fragmented CDR governance becomes more pronounced. The absence of a global certification framework deepens distrust between high-income and lower-income countries, while CDR quality standards become sites of geopolitical contestation. Advanced MRV regions (such as North America and Europe) impose strict integrity standards that block removals from less-developed systems, fragmenting markets, while reliance on future removals heightens moral hazard by lowering urgency for current mitigation.

Technologically advanced regions, including the United States, the Nordics, Japan and the United Kingdom, consolidate innovation clusters and strengthen domestic CDR industries. Meanwhile, lower-income, land-rich countries in the Global South increasingly host large-scale, land-based CDR projects that proceed with limited community consent, weaker regulatory oversight and insufficient compensation, reinforcing patterns of “carbon colonialism” (see Appendix).46 Civil society critiques intensify, framing this dynamic as “green neocolonialism,” where wealthier states externalize removals while retaining economic and regulatory control.

2041–2050: Bloc Convergence, Interoperability Pilots and Limited Realignment

From 2041 to 2050, CDR governance may converge regionally, despite the absence of global harmonization. Cost reductions and private-sector incentives could support interoperable certification and transparent MRV systems, while Indigenous-led, municipal and regional governance embed community-led CDR into regional planning. Cooperation among like-minded blocs might support alignment on verification standards, definitions and benefit-sharing to reduce transaction costs, facilitate cross-border credit trade and enhance market credibility, suggesting bottom-up convergence rather than global mandates.

Early signals of this trajectory may include proposals for a Global CDR Quality Index, mutual recognition of certification standards, and pilot projects for interoperable MRV systems and shared CO₂ storage. Consistent with current trends in CDR governance and market development, deployment outcomes would likely depend on equitable finance, technology access, local capacity and community consent.

Despite these advances, fragmentation and uneven deployment may persist without coordinated national and intergovernmental political commitment. Although local and regional actors may spur innovation, without formal authority over cross-border accounting, large-scale finance and credit integrity disputes, convergence efforts may struggle to scale. Ultimately, without a unified global framework, carbon removal risks shifting from a shared environmental necessity to a competitive geopolitical asset.

By 2050, the regional hub model could entrench a world of technological “haves” and “have-nots,” where a few powerful blocs control access to advanced CDR technologies and infrastructure. In the present context, rising geopolitical tensions (such as US–China competition, energy insecurity in Europe, and conflicts in the Middle East and Ukraine) threaten to turn carbon removal into a tool of strategic leverage rather than a global public good.

As technology is increasingly friend-shored and national security priorities dominate climate policy, access to CDR technologies, certification systems and carbon markets may become increasingly fragmented. This dynamic may not only inflate transaction costs but also risk undermining the Paris Agreement’s collective ambition, replacing global cooperation with a zero-sum system of carbon diplomacy that entrenches inequities and leaves vulnerable regions bearing the brunt of climate impacts.

SCENARIO 3

Market-driven, Technology-led Race — Private Sector Dominance

In this scenario, CDR scales primarily through private-sector initiative, supported by profit motives, competitive positioning and technological breakthroughs rather than coordinated state-led governance. Global investments total roughly $32 billion: $21 billion in engineered solutions and $11 billion in nature-based approaches, with private capital ($17 billion) surpassing public funding ($15 billion). Market projections indicate the CDR credit market could reach $100 billion annually by 2030–2035, yet demand must grow three- to fivefold to sustain current investment levels. Persistent barriers, including unclear guidance on removals and the absence of widely accepted quality standards, limit broader uptake.47

2025–2030: Early Market Momentum, Concentration and Policy Volatility

In the late 2020s, CDR growth is driven mainly by corporate net zero pledges (highlighting both the concentration of innovation in advanced economies and the dominance of voluntary rather than government-mandated procurement48), innovative finance instruments and a diversifying investor base (including sovereign wealth funds and asset managers, whose participation suggests longer-term investment horizons and strategic positioning ahead of broader market recognition).49 Early-stage private capital for carbon removal solution developers reached roughly $838 million in 2023, vastly outpacing public grants of about $24 million.50 While this concentration accelerates technological learning, it also creates vulnerability if corporate demand declines.

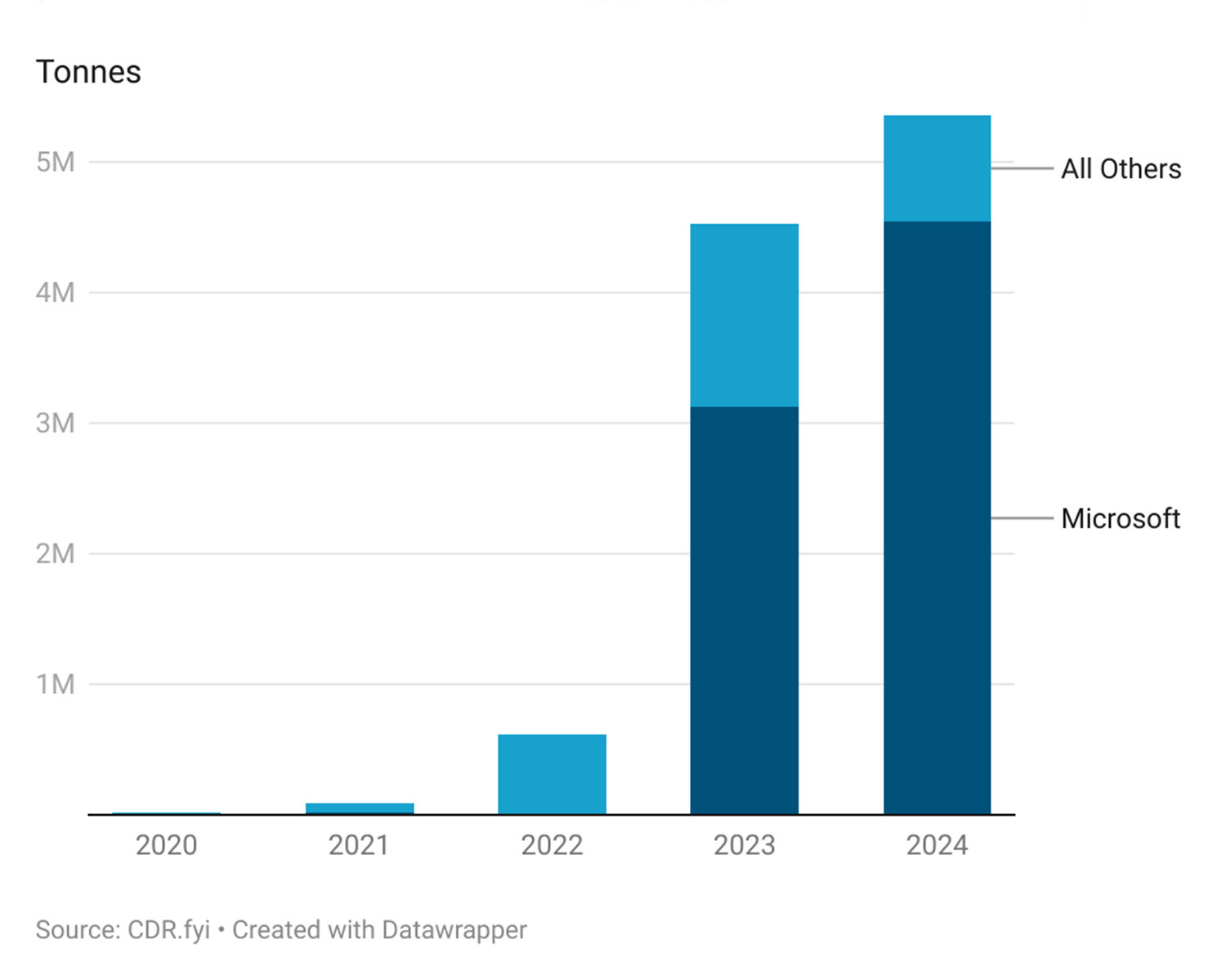

Figure 1: Durable CDR Purchase Volumes, 2020–2024

This dynamic does not imply the disappearance of free-riding incentives; rather, some firms treat early access to high-quality removal credits as a strategic hedge against future regulatory requirements, supply constraints and reputational risks associated with net-zero commitments, while also using a portfolio approach across multiple projects to build market knowledge, secure supply and enhance corporate climate leadership.51

The global voluntary carbon market nearly quadrupled in value from 2020 to 2021 (reflecting surging corporate interest in carbon credits, including, but not limited to, durable carbon removal), reaching approximately $2 billion.52 Blockchain-enabled crediting is beginning to reshape market tracking, yet concerns over transparency highlight the need for integrity-focused governance.53 Meanwhile, policy volatility, such as the US Department of Energy’s 2025 cancellation of $3.7 billion grants for clean energy projects, reinforces uncertainty for investors.54

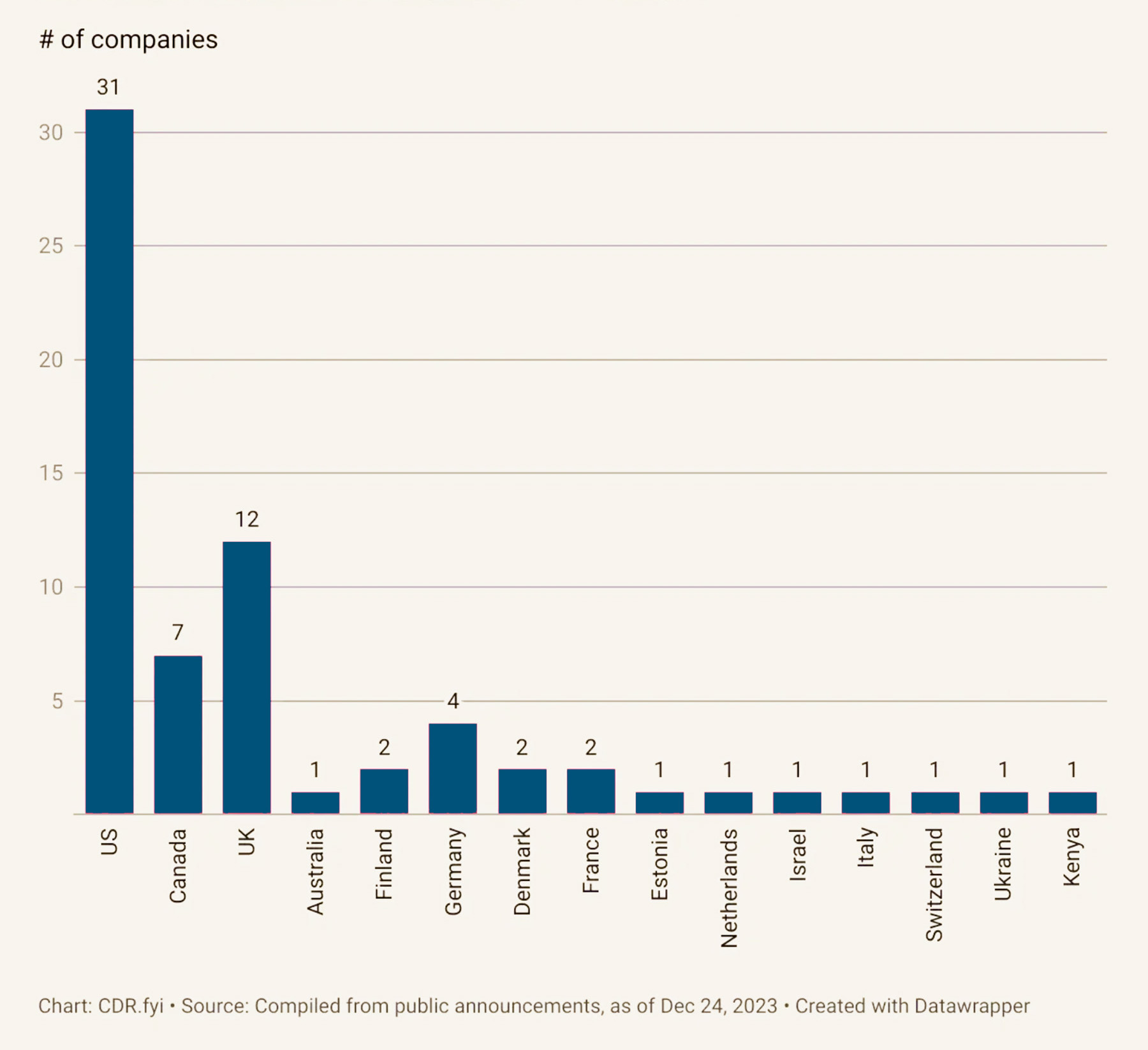

Figure 2: 2023 Investment in All CDR by Country

By 2030, private-sector activity is expected to drive growth in voluntary carbon markets, although overall deployment remains uneven across countries, following previous trends (Figure 2).55 Overall, the period reflects both promise and fragility: market forces can drive early scaling, yet without robust governance, oversight and equitable participation, CDR deployment may remain uneven, concentrated and vulnerable to moral hazard.

2031–2040: Scaling, Techno-commercial Learning and Governance Stress

During the 2030s, DAC and BECCS may achieve cost reductions through learning and scale, yet estimates ($126 to $1,900 per tonne CO₂) remain above the $100 per tonne threshold for mass deployment. As a result, market expansion remains uneven and dependent on policy incentives and a small number of major corporate buyers.

Weak signals include expanding CDR activity in the United States and the European Union, and the growth of long-term corporate offtake agreements. Key signposts include increasing investment flows and techno-commercial learning, although new financing mechanisms remain uncertain and unevenly distributed.56 Investment remains concentrated in the United States and Europe, while uneven verification systems and registry standards continue to undermine credit integrity.57

These dynamics suggest that even with falling costs, reliance on a few major buyers, policy volatility and geopolitical fragmentation underscore that CDR scaling requires resilient governance, diversified investment and cross-border coordination.

2041–2050: System Maturity or Entrenched Inequality

By the 2040s, the carbon removal market could either consolidate into an efficient industry or become concentrated among a small number of dominant firms. With technological learning and scale, BECCS and DAC could fall to a few hundred dollars per tonne of CO₂.58 However, even if several gigatonnes are removed annually by 2050, benefits may accrue disproportionately to advanced economies and major firms, raising concerns regarding equity, moral hazard and climate justice.59 Thus, a market-first approach risks turning carbon removal into a private luxury rather than a global public good. This trajectory could create a stark “carbon divide,” where wealthy nations and major firms capture technological gains while the rest of the world bears the consequences of climate change.

Although competition may reduce removal costs, it cannot ensure equity. Moreover, persistent geopolitical tensions may heighten uncertainty, restrict technology access and weaken policy coordination by challenging the credibility of large-scale CDR efforts in the near future.

Conclusion

Although policy signalling for carbon removal is increasingly emerging from multiple sources — including commitments under the Paris Agreement, corporate net-zero pledges targeting 2050, and policy initiatives such as the European Green Deal60 — sustaining long-term political and economic support for large-scale deployment remains a key governance challenge.

Across the three scenarios, a clear insight emerges: institutional strength and governance are at least as critical as technological capability in scaling CDR. The centralized governance pathway offers the strongest potential for equitable standards and coordinated scaling, but risks slow implementation and political gridlock. The fragmented regional model enables tailored solutions and local innovation, yet uneven verification and interoperability challenges could compromise credit integrity. The market-driven, technology-led race promises rapid cost reductions and capacity growth, but without safeguards it risks deepening inequities, moral hazard and corporate concentration.

Given current trajectories, a hybrid outcome appears most plausible, which is a blend of private innovation with regional coordination. However, without deliberate governance interventions, the default path may concentrate benefits among wealthy nations and major firms, creating a carbon divide and undermining climate justice. Large-scale CDR deployment requires selective multilateral oversight and regulatory mechanisms to mitigate inequities and ensure accountability.

These pathways assume a relatively stable political commitment to climate mitigation, an assumption that is becoming increasingly uncertain. Growing geopolitical fragmentation, domestic backlash against climate policy and weakening multilateral institutions could slow the scaling of CDR or shift attention toward alternative interventions such as solar geoengineering. Nevertheless, several emerging weak signals suggest that carbon removal may continue to advance. For instance, private-sector advanced market commitments, including Frontier Climate’s $1-billion pledge launched in 2022 and subsequent early offtake agreements, are beginning to generate demand signals and de-risk investment for CDR technologies.61 Similarly, the integration of carbon removal into agricultural systems, through approaches such as enhanced rock weathering, shows promise for scalable land-based removal, with emerging research suggesting potential co-benefits for soil health, crop yields and smallholder farmers, particularly in countries such as India and Brazil.62 In addition, youth climate activism through global networks such as YOUNGO, the official youth constituency of the UNFCCC, signals growing normative support that may shape long term policy engagement with CDR.63

These developments indicate that the future of CDR governance may not fully align with any single scenario outlined above, or even a hybrid of them. Instead, governance may evolve through more complex and adaptive pathways in which non-state actors, including corporations, civil society networks, research institutions and youth movements play a greater role in shaping policy agendas, standards and accountability mechanisms.

In this context, the foresight approach adopted in this research is particularly valuable. By analyzing emerging drivers, weak signals and signposts, the study identifies plausible trajectories for CDR governance and demonstrates how early indicators can inform anticipatory policymaking. Such governance, grounded in monitoring weak signals, strengthening institutional legitimacy, and embedding accountability mechanisms, will be essential to ensure that CDR remains aligned with equitable and sustainable climate objectives in an increasingly unstable global landscape. Ultimately, the future of CDR will depend not only on technological capacity but on how effectively institutions, markets and societies govern these capabilities in a fair and accountable manner.

Acknowledgement

I would like to sincerely thank all reviewers for their valuable feedback and thoughtful comments, which significantly improved this work. I am especially grateful to Dr. Carrie Wright for encouraging me to publish this paper.

APPENDIX

Potential Negative Impacts of Inequitable CDR Deployment

| Impact Area | Consequences | Global South Vulnerability |

| Economic | Dependency on external technology, lost innovation, unequal benefit sharing | High (limited capital, infrastructure) |

| Social | Displacement, land conflict, increased inequality, diminished autonomy | High (existing vulnerabilities) |

| Environmental | Ecosystem degradation, resource depletion, inappropriate technology use | High (fragile ecosystems, climate stress) |

| Political | Weakened negotiation position, carbon colonialism, reduced global cooperation | High (historical power imbalances) |

Source: PRISM Scenario Explorer.