Expanding the use of hydrogen on a vast scale has gained increasing attention over the past two decades, although use of hydrogen for industrial purposes has been well established for more than a century. The current focus on green hydrogen produced from clean (non-carbon) primary sources is largely driven by the broader challenge of decarbonizing the global economy. Green hydrogen has enormous potential for advancing a low-carbon future within the hard-to-abate sectors and also for shaping the issue of energy security. Thus, approximately 70 countries have developed national hydrogen strategies or roadmaps. In this paper, we present a beginner’s guide for policymakers and readers interested in green hydrogen. We address the following key questions: What are the critical steps, developments, strategies and policies for expanded use of green hydrogen in various applications? What are the related challenges of governance and policies to help accelerate deployment of green hydrogen technologies on a global scale? We have also developed an alternative governance model for a green hydrogen ecosystem.

Background

Hydrogen is the first element on the periodic table and has a higher energy content per kilogram than other fuels. Its higher heating value (HHV) is 141.7 MJ/kg, compared to around 55 MJ/kg for methane (natural gas) and 46 MJ/kg for gasoline.1 The HHV of hydrogen represents the total energy released during combustion, including energy from condensing water vapour. Regarding energy content by weight, hydrogen’s HHV is approximately 2.5 times that of gasoline and about 2.6 times that of methane. This means that, theoretically, a hydrogen-powered vehicle could travel up to 2.5 times farther than a gasoline-powered car on an equivalent weight of fuel, although practical efficiencies depend on specific fuel systems. However, hydrogen has a very low density of approximately 0.09 kg/m³ at 1 bar (the standard pressure used to measure gases) and 0°C, which introduces a unique challenge for storage and distribution of hydrogen: about 11,000 litres of hydrogen is required to store it at atmospheric pressure. Hydrogen also does not exist freely in nature, so it must be produced from various sources using different production methods. Current global hydrogen is primarily produced through reforming technologies that rely on fossil fuels, such as coal and natural gas. At the end of 2021, nearly 47 percent of global hydrogen production came from natural gas, 27 percent from coal, and 22 percent as a by-product of oil, with only about four percent produced through electrolysis, a process that uses electricity to split water into hydrogen and oxygen.2 Since the global electricity supply had an average renewable share of around 33 percent in 2021, only about one percent of the world’s hydrogen output was generated using renewable energy sources.3

Most hydrogen production is currently generated from fossil fuels, with a global capacity of approximately 0.1 gigatonnes annually.4 Fossil-fuel-based hydrogen serves as a feedstock in industries such as oil refining, fertilizer production and various downstream chemical processes. Fossil-fuel-based hydrogen, although cost effective, is not a sustainable solution, as current hydrogen production is responsible for annual CO2 emissions between 1,100 and 1,300 megatonnes.5 This is a significant contributor to climate change. The emissions from hydrogen generation vary widely depending on the production method, with “grey” hydrogen derived from fossil fuels resulting in the highest CO2 emissions.

“Blue” hydrogen, also derived from fossil fuels, incorporates carbon capture and storage to decrease CO2 emissions, but its technical and economic feasibility remains an open question.

Green Hydrogen

In this paper, we focus on sustainable or “green” hydrogen, produced using renewable energy-powered electrolysis with no direct emissions. It should be noted that relying solely on general colour classifications is not recommended for policymakers because it overlooks the lifecycle costs and emissions profiles associated with different hydrogen production methods.6 For instance, hydrogen produced from wind, concentrated solar power (CSP), and solar photovoltaics (PVs) are all categorized as green hydrogen, although their lifecycle carbon emissions differ significantly. The lifecycle CO2 emissions of hydrogen from wind, CSP and solar PVs are 13.5, 28.1 and 43.6 gCO₂/kWh, respectively.7 Nonetheless, for simplicity, this paper will use the term “green hydrogen” to refer to clean hydrogen with low lifecycle carbon emissions.

Many countries have investigated hydrogen for various uses in the past, but lately, green hydrogen has captured global interest. The main drivers of this interest in green hydrogen can be listed as:8

- Decarbonization goals: Green hydrogen is pivotal for sectors that are hard to decarbonize, such as ammonia production and steel manufacturing.

- Industrial development: Green hydrogen can spur growth in hard-to-abate industries and support local manufacturing of hydrogen tech, boosting competitive green industrialization, particularly in the Global South.

- Energy export and security: Green hydrogen opens up new export possibilities, especially for countries rich in renewable energy. It can also improve energy security by reducing fossil fuel imports and widening the range of energy suppliers.

- Renewable storage: Green hydrogen can help store renewable energy for the long term, which is useful when there is more electricity than needed.

- Air quality: In transportation, hydrogen fuel cells can reduce air pollution, which is especially useful for heavy-duty vehicles.

- Food security: Green hydrogen can help stabilize fertilizer prices and support local farming, which is important in countries such as Kenya, where fertilizer supply is significantly affected by natural gas prices.

Energy security is one of the major drivers behind the growing interest in green hydrogen, in particular for countries heavily dependent on imported fossil fuels. Global events have led to volatile oil and natural gas prices, as shown in Figure 1. Price volatility has caused a significant risk to energy security for nations dependent on foreign fossil fuels, such as Germany.

Fluctuating energy prices have also affected other sectors, such as agriculture. For instance, ammonia — essential for fertilizer production — requires hydrogen as a key input that has recently been mainly produced from natural gas. The Russian invasion of Ukraine in 2022 has driven energy prices even higher, pushing up fertilizer costs by 70 percent in Kenya in 2022.9 It was estimated that this surge in fertilizer prices could lead to a 12 percent drop in maize yields, equivalent to approximately 400,000 tonnes less maize production.10

Developing local green hydrogen production can therefore help enhance energy security resilience by reducing reliance on imported fuels and stabilizing critical supply chains. Yet the main challenge of using green hydrogen remains its high production cost. Thus, green hydrogen production should be supported by well-structured policies, as described in the next section of this paper.

Figure 1: Inflation-adjusted and Energy-adjusted Oil, Gas and Coal Prices in the United States

Source: Adams.11

The rest of this paper investigates current hydrogen strategies and policies, examines challenges in hydrogen governance, and discusses an alternative governance model for a green hydrogen ecosystem. Policymakers should consider various factors for effective green hydrogen governance and policies. Table 1 outlines various studies on green hydrogen. The table can be a starting point for policymakers interested in green hydrogen governance and policy.

Table 1: Overview of Key Studies on Green Hydrogen:

Eco-Technoeconomic, Governance, Policy and Future Outlook

| Source | Type of Study | Key Topics | Main Focus | Relevance to Hydrogen Governance |

| “What governs the transition to a sustainable hydrogen economy? Articulating the relationship between technologies and political institutions”12 | Policy Governance | Covers paradigms of governance, the influence of institutions, and the complexity of transitioning to a hydrogen economy. | Examines four governance paradigms (policy networking, government, corporate business, and challenges) and their influence on the hydrogen economy transition. | Highlights the importance of aligning policy frameworks with technological innovation, emphasizing the need for nuanced governance models for hydrogen transitions. |

| “National Hydrogen Strategies”13 | Working Paper | Covers issues such as varying national strategies, the hydrogen colour debate, demand-focused approaches, and economic potential related to workforce development. | Examines the need for flexibility in national hydrogen strategies, pushing back against a uniform approach. Stresses the importance of exploring demand-side factors and establishing a diverse hydrogen economy. | Underscores the importance of a tailored global approach to hydrogen strategies, advocating for multi-stakeholder dialogue and recognizing country-specific hydrogen potential and requirements. |

| “Global trade of hydrogen: What is the best way to transfer hydrogen over long distances?”14 | Working Paper | Focuses on hydrogen carriers, long-distance transportation challenges, comparative analysis of techno-economic factors, and global trade implications. | Evaluates and compares the viability of liquid hydrogen, ammonia, methanol and methylcyclohexane as hydrogen carriers for long-distance transport, addressing efficiency, cost and potential limitations for each. | Highly relevant to policymakers as it comprehensively assesses long-distance hydrogen transport options, which are crucial for establishing effective hydrogen trade policies and international hydrogen supply chains. |

| “From Hydrogen Hype to Hydrogen Reality: A Horizon Scanning for the Business Opportunities”15 | Working Paper | Focuses on the viability of hydrogen business opportunities. | Assesses 20 hydrogen-related business opportunities globally while examining 64 companies’ business models. | Provides valuable insights into the commercial aspects of hydrogen, helping policymakers understand which applications could be integrated into sustainable governance frameworks and the overall hydrogen economy. |

| “Future costs of hydrogen: a quantitative review”16 | Review Paper | Covers hydrogen production costs, regional cost differences and long-term cost forecasting. | Aggregates cost projections from various studies to present future trends in hydrogen production costs. It emphasizes the cost competitiveness of electrolysis over time and regional differences in production costs. | Provides a critical understanding of hydrogen cost trends, which aids policymakers in crafting supportive policies and planning investment strategies based on anticipated cost reductions and regional competitive advantages. |

| “Future hydrogen economies imply environmental trade-offs and a supply-demand mismatch”17 | Research Paper | Uses hydrogen demand scenarios to examine environmental trade-offs, resource constraints and supply-demand mismatches. | Analyzes four hydrogen demand scenarios for 2050, highlighting potential environmental impacts, supply-demand mismatches and the challenges of upscaling production. | Provides insights into long-term planning for hydrogen economies, emphasizing the need to address regional supply-demand gaps and resource limitations in policy frameworks. |

| “International co-operation to accelerate green hydrogen deployment”18 | Brief Report | Includes global collaboration efforts, supply and demand challenges, and international coordination. | Focuses on the insights gathered from the International Renewable Energy Agency’s (IRENA’s) Collaborative Framework meetings in 2023, addressing the state of green hydrogen deployment and the strategies to ramp up supply and demand globally. | Highlights the critical role of international cooperation in accelerating green hydrogen deployment by fostering global collaboration, harmonizing standards and supporting policy frameworks. The report underscores the importance of coordinated efforts to overcome deployment challenges, align regulations and facilitate market development for green hydrogen at a global scale. |

| “Green hydrogen strategy: A guide to design”19 | National Hydrogen Strategies and Policy Guide Report | Examines policy drivers, stakeholder engagement, strategic design and long-term planning. | Provides a comprehensive guide for policymakers on developing green hydrogen strategies, including target setting, priority areas and addressing barriers. | Supports national governments in structuring effective hydrogen policies, crucial for aligning hydrogen development with decarbonization and energy transition goals. |

| “Synthetic natural gas as a green hydrogen carrier — Technical, economic and environmental assessment of several supply chain concepts”20 | Research Paper | Addresses hydrogen carriers, synthetic natural gas and the efficiency and emissions implications of various supply chain setups. | Analyzes synthetic natural gas as a hydrogen carrier by assessing the technical and economic aspects, specifically focusing on CO₂ sourcing and reforming options to enhance efficiency and reduce emissions. | Provides a detailed evaluation of synthetic natural gas’s potential role in hydrogen transport, relevant for policymakers considering hydrogen infrastructure that leverages existing natural gas networks. |

| “Renewable hydrogen standards, certifications, and labels: A state-of-the-art review from a sustainability systems governance perspective”21 | Review Paper | Focuses on standards and certifications, sustainability, systems governance and global coordination. | Examines the diverse approaches to hydrogen certification, identifying challenges posed by fragmented standards and advocating for a unified approach that balances economic, social and environmental considerations. | Provides a framework for policymakers and industry leaders to consider in developing global standards, crucial for supporting sustainable hydrogen markets and facilitating international cooperation. |

Current National Strategies and Policies for Green Hydrogen

As explained in a report from IRENA,22 by May 2024, 46 countries and regions had completed and released their hydrogen strategies, along with eight detailed roadmaps. Additionally, at least 20 more nations were working on or preparing to publish their plans. This surge in global interest means that at least 74 countries are already engaged in planning the future of the clean hydrogen industry, a promising sign for the future of clean energy. Various strategic documents provide a clear overview of the national goals for developing a green hydrogen sector, both within the country and globally. They discuss elements such as sector-specific demand, production levels, the economy, export potential, standards, certifications and associated challenges and opportunities. Therefore, different countries have created their hydrogen strategies with a range of priorities while considering their specific energy resources, economic goals and environmental challenges. The focus areas for hydrogen use also differ widely from one nation to another.

We can summarize the national hydrogen strategies of several key countries based on reports from the World Energy Council23 and IRENA24 as follows.

Japan and South Korea are building hydrogen economies to reduce their dependence on imported energy. Japan focuses on small, decentralized power generation with home fuel cells (devices that produce electricity by using green hydrogen, with water as the only by-product), called the “ENE-FARM” system, which produces electricity and hot water. South Korea is taking a broader approach, focusing on both central power generation and home fuel cells. Both nations are investing heavily in fuel cell vehicles in the transportation sector, with South Korea aiming to become a global leader in hydrogen-powered vehicles and expand into export markets. These strategies reflect a shared goal of finding innovative domestic solutions to cut down on energy imports, in particular within the power and transport sectors.

Australia is taking a different path, focusing on producing hydrogen for export and exploring its use in domestic heavy-duty and long-distance transport. Clean ammonia production at a large scale is also part of its plan.

In Europe, the primary goal is to decarbonize industries and transportation, increasing the use of renewable energy despite limited capacity. Germany is interested in industrial applications such as chemical manufacturing, steel production and heavy transport. France aims to phase out carbon-based hydrogen in its industries and is also looking into hydrogen’s potential in maritime applications and aviation. Spain and Portugal aim to implement green hydrogen for local consumption while setting their sights on future exports.

Norway is more cautious, focusing on producing hydrogen near its primary consumers while using CO₂ storage to make it cost effective.

In the Americas, Chile is replacing imported ammonia with locally produced green hydrogen for transport, thanks to its abundant solar resources. Canada focuses on hydrogen for short-term transport needs, such as fuelling buses, delivery trucks and forklifts, as well as blending hydrogen with natural gas to decarbonize heating.

Many countries have also been working on policies to support green hydrogen implementation. Although there are differences in public policy support of the countries to support green hydrogen implementation in the clean energy transition, we can categorize the hydrogen policies into four key areas.25

- Establishing objectives and providing clear long-term policy direction.

- Stimulating demand for hydrogen with low-carbon emissions.

- Minimizing investment risk.

- Encouraging research, innovation, strategic pilot projects and the exchange of knowledge.

Canada’s policy ecosystem, which reflects these key areas, includes the following initiatives.26

- The Clean Hydrogen Investment Tax Credit offers credits of between 15 and 40 percent for clean hydrogen projects, with the cleanest projects receiving the highest support.

- Additional tax credits, such as the Clean Electricity Investment Tax Credit and Clean Technology Manufacturing Investment Tax Credit, provide credits of up to 30 percent to help reduce costs for electricity generation systems and hydrogen equipment.

- The Investment Tax Credit for Carbon Capture, Utilization and Storage offers up to 60 percent for carbon capture technology, benefitting hydrogen produced from natural gas.

- Canada supports hydrogen production through the Clean Fuels Fund ($1.5 billion), the Net Zero Accelerator ($8 billion) and the Canada Growth Fund ($15 billion), which aim to scale up hydrogen projects.

- The Canada Infrastructure Bank finances hydrogen-refuelling infrastructure.

- The Zero Emission Vehicle Infrastructure Program funds hydrogen-refuelling stations and zero-emission vehicles.

- Canada’s Clean Fuel Regulations incentivize hydrogen use in transportation and industrial sectors by establishing a credit market.

- Canada’s carbon pollution pricing system encourages low-carbon hydrogen projects, in particular for high-emissions industries such as steel and ammonia production.

Green Hydrogen Governance and Policy Challenges

Green hydrogen implementation faces numerous challenges, but the governance and policy issues can be distilled into two major problems: first, how to balance the long-term demand for hydrogen with the urgent need for decarbonization; and second, how to create policies that enable different stakeholders to share critical data and collaborate more effectively.

The first challenge lies in balancing the long-term demand for hydrogen with the urgent need for decarbonization. Currently, the immediate focus is on decarbonizing the electricity grid, deploying heat pumps and scaling up electric vehicles.27 This means there is limited demand for clean hydrogen in the short term. However, looking ahead, clean hydrogen will be crucial for industries such as steel production, ammonia synthesis and heavy transport. This makes it essential to develop the hydrogen sector now to ensure it is ready when large-scale demand emerges.28

Meeting this future demand will require a vast amount of clean electricity. For instance, using clean hydrogen solely for steel production would demand 134 percent of all global wind and solar capacity — essentially 1.34 times the total current renewable infrastructure.29 Expanding hydrogen use to other applications, such as clean ammonia production, aviation and shipping, will require even greater levels of renewable energy. This presents a significant governance and policy challenge, as the effort to scale up hydrogen production must be carefully balanced with ongoing electrification efforts for decarbonization.

The barriers to green hydrogen production can be categorized into four main areas: technological, economic, institutional and social.30 Table 2 summarizes the specific issues related to these barriers. For example, economic challenges include the high costs of green hydrogen, insufficient demand, limited end-use applications, first-mover disadvantages and a shortage of skilled personnel. As shown in Table 2, each of these barriers is interconnected with the others.

Table 2: Main Barriers to Green Hydrogen and their Associated Issues

| Technological |

|

| Economic |

|

| Institutional |

|

| Social |

|

Source: IRENA.31

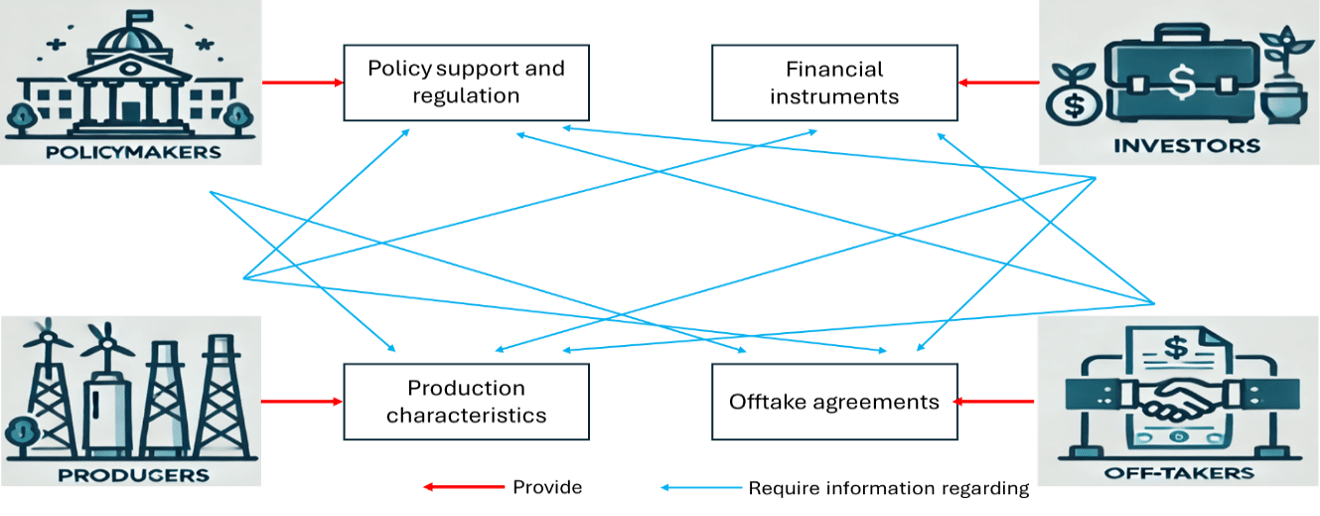

This interconnectedness creates a complex situation in which different stakeholders may focus on addressing specific issues but still require information, data or commitment from others, who often work on different challenges. This lack of coordination and data-sharing among stakeholders can hinder overall progress, a phenomenon identified in a 2024 IRENA report as the “green hydrogen deadlock,” depicted in Figure 2.32

Figure 2: The Green Hydrogen Deadlock

Source: IRENA.33

These intertwined barriers highlight a central governance challenge: establishing policies that facilitate effective data-sharing and stakeholder collaboration. This challenge is at the core of the second issue, that of enabling better coordination and information flow to accelerate green hydrogen development.

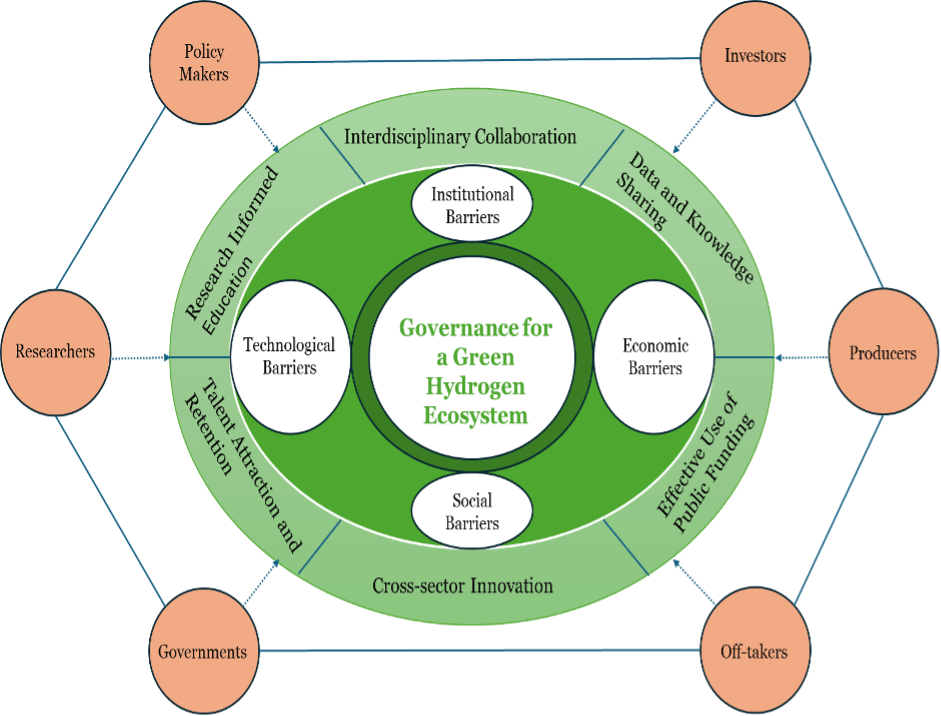

An alternative governance model that actively involves researchers, industry and policymakers in a collaborative, data-driven process is needed to address these two challenges. To fill this gap, we propose a concept called Governance for a Green Hydrogen Ecosystem. The preliminary framework for this model, along with future development plans, is detailed in the next section.

Governance for a Green Hydrogen Ecosystem and Future Work

In the previous section, we summarized the critical barriers to a successful implementation of green hydrogen within the economy into two major challenges. A convergence of efforts by different actors, enabled by government policy incentives and early-stage financial support to promising green hydrogen projects and leading entries, would be necessary.34 We describe below an operational model for effective use of public funding.

Traditionally, addressing the challenges related to governance of emerging green hydrogen technologies has centred around four main models: governance by policy networks; governance by corporate business; governance by government; and governance by challenge.35,36 Of these models, governance by government has been the dominant approach.37 In light of the two major challenges described in the previous section, we propose an alternative model that focuses on an ecosystem view and addresses the myriad intersectoral and intersectional linkages of the entire green hydrogen ecosystem, from production to transport to end user. This perspective provides better insights into the influences and the strength of feedback loops within the overall system.

Our ultimate goal is to ensure that public funds are used effectively to advance an important societal objective of decarbonization through the green hydrogen pathway, while minimizing the inherent risks associated with emerging technologies. An ecosystem-driven approach to green hydrogen governance is essential for achieving this goal, as it can foster innovation and generate valuable by-products. This approach mirrors past investments in space exploration, where high initial costs drew criticism. NASA, for example, faced intense scrutiny over its spending. However, its research ultimately led to significant technological advancements,38 such as solar PVs,39 which are now critical to renewable energy systems. Just as NASA’s investments spurred cross-sector innovation, a similar approach to green hydrogen could drive technological advancements across multiple sectors.

The proposed governance model aims to facilitate these changes and requires the active participation of all stakeholders. Figure 3 illustrates our alternative governance model for green hydrogen, showcasing the core elements and interactions within the proposed ecosystem. The model’s primary mechanism is facilitating collaboration among diverse stakeholders — policymakers, investors, producers, off-takers, governments and researchers — as shown in the outermost layer. These stakeholders are essential for fostering interdisciplinary collaboration, data-sharing and knowledge-sharing — as represented in the middle layer. This collaborative focus empowers cross-sector innovation, talent attraction and retention, effective use of public funding, and the development of research-informed educational pathways.

The arrows in Figure 3 indicate the flow of influence and interactions between stakeholders, illustrating how these collaborations can address the interlinked technological, economic, institutional and social barriers specific to the green hydrogen ecosystem, as depicted in the innermost layer.

Figure 3: General Framework of Governance for a Green Hydrogen Ecosystem

Source: Authors.

We plan to develop this governance model further in future work, focusing on understanding the direction and magnitude of influence within the ecosystem to maximize green hydrogen’s impact. Additionally, we aim to develop potential solutions to address intellectual property (IP) and collaboration risks within this governance model. Two main issues need consideration: maintaining competitive IP and managing IP in a globalized market. Engaging multiple players, as emphasized in our model, makes protecting IP a complex governance issue. Furthermore, there is a risk of IP being replicated or modified by other entities, in particular in regions with less stringent protections, potentially allowing competitors — or even partners — to develop similar technologies and enter the market. In future papers, we will explore policy and governance solutions to these issues as we expand the model of Governance for a Green Hydrogen Ecosystem.

Authors’ Note: In some paragraphs, the authors used ChatGPT 4.0 and Grammarly to enhance readability, clarity and word choice. After applying these tools, the authors reviewed the content thoroughly and took full responsibility.